Instacart went public in September 2023 at $30 per share, giving the company a market cap of about $9.3 billion. Shares briefly ran up to $42 on the first day before closing around $33.

To understand why this IPO is interesting, it helps to understand what kind of business Instacart actually is.

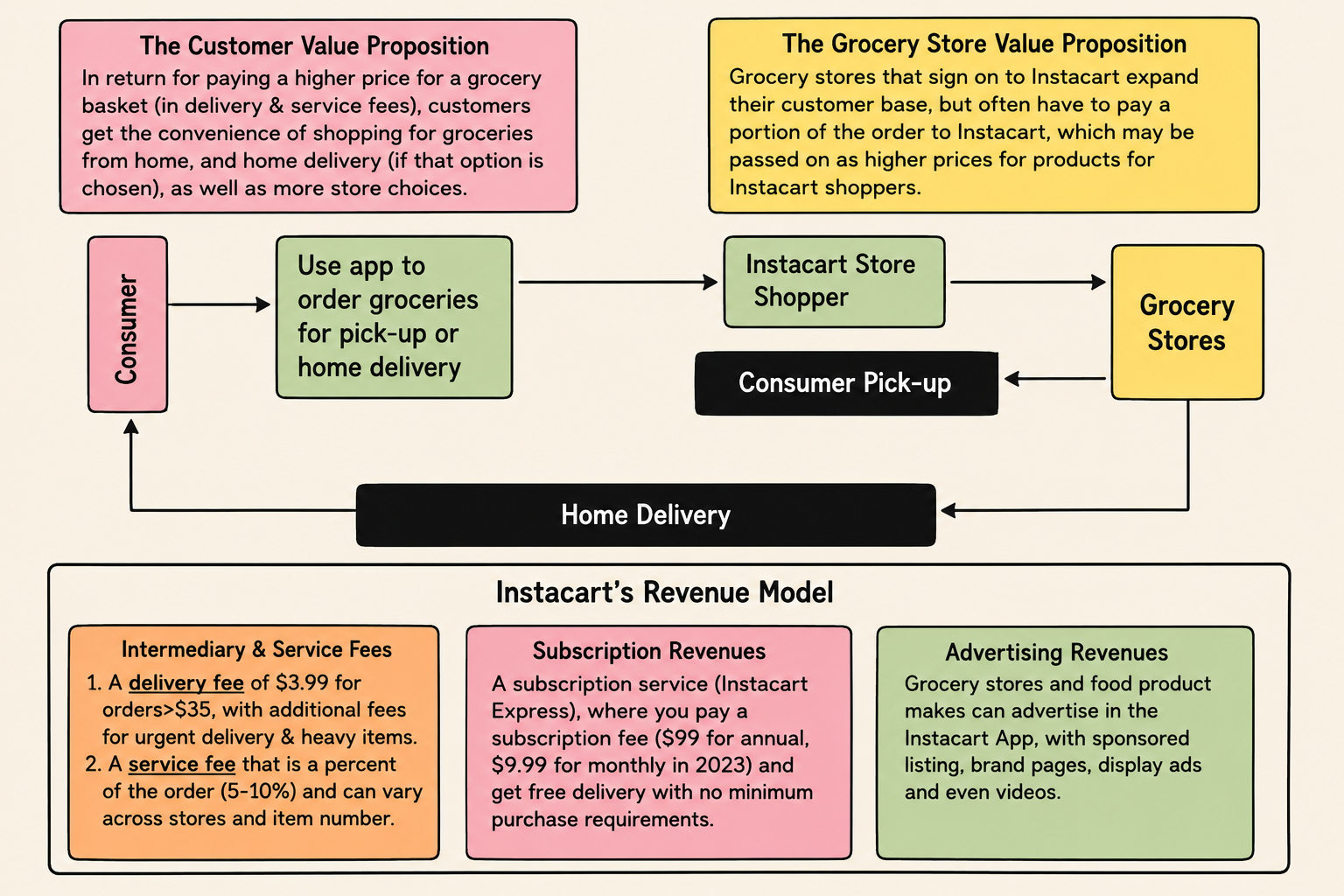

A three-sided marketplace in a low-margin industry

Most marketplaces connect two groups: buyers and sellers. Instacart connects three.

There are customers ordering groceries. There are grocery stores and restaurants supplying the inventory. And there are independent shoppers who physically pick and deliver the orders. Each group only shows up because the other two are already there. Customers come because there are good stores and reliable shoppers. Shoppers come because there are enough orders to make it worth their time. Stores come because there are enough customers. This is the classic marketplace chicken-and-egg problem, but with an extra leg.

Instacart earns revenue from several places: delivery and service fees from customers, commissions from grocery partners, advertising fees from brands that want visibility on the platform, and subscriptions from Instacart+ members who pay a monthly fee for free delivery.

The advertising business is worth paying attention to. Grocery is a notoriously low-margin industry. Stores run on thin margins, which limits how much Instacart can take from each transaction. Advertising is where the platform can make real money, because brands will pay a premium to be seen at the moment someone is already shopping. It's similar to how Amazon generates outsized profit from ads relative to its retail business.

What the IPO numbers actually mean

When a company goes public, it sells shares at a fixed price to raise money. That price multiplied by the total number of shares outstanding gives you the market cap, which is essentially what the market collectively says the whole company is worth at that moment.

At $30 per share with 310 million shares, Instacart's market cap was $9.3 billion.

That number matters because it determines how every investor did. If you put money in when the company was valued at $75 million and it exits at $9.3 billion, your return is enormous. If you put money in at a $13 billion valuation and it exits at $9.3 billion, you lost money.

This is exactly what happened.

Who won and who lost

Y Combinator and Khosla Ventures invested in Instacart's seed round in 2012, when the company was valued at $75 million. At the IPO valuation of $9.3 billion, their return was over 12,000%. That is not a typo.

The investors who lost money were the most recent ones. Fidelity and T. Rowe Price came in during later rounds at much higher valuations. When the IPO priced below what they paid, they were underwater.

Sequoia Capital is the most interesting case because they invested multiple times. They led the Series A in 2013 at the same $75 million seed valuation, then invested again in a later round at a $5.78 billion valuation. Their later bets lost money, but their early bets made so much that the overall picture is still very good. Notably, Sequoia bought another $400 million of shares on the day of the IPO itself, a signal that they believed the stock had room to grow even at the public price.

Andreessen Horowitz entered during the Series B in 2014 at a $930 million valuation. By the time of the IPO, they had roughly a 900% return on that investment.

The pattern here is the classic venture capital dynamic. Early investors take the most risk, when the company is young and unproven, and earn the highest returns if it works out. Later investors get more certainty but pay for it with a higher entry price. When a company's valuation peaks in private markets and then comes down at IPO, the later investors absorb the loss.

What bookrunners do and what they earned

Before a company can sell shares to the public, it needs someone to manage the process. That role falls to underwriters, commonly called bookrunners.

The bookrunner's job is to help the company figure out what price to set for its shares, find institutional buyers willing to purchase them, and coordinate the mechanics of the actual sale. Goldman Sachs and JP Morgan were the lead bookrunners on Instacart's IPO.

The bookrunners don't just facilitate. They buy shares themselves as part of the deal and then sell those shares to investors. For each share they place, they earn a fixed fee.

Goldman took on roughly 9.68 million shares and earned $1.65 per share in fees, totaling about $16 million from that portion of the deal. JP Morgan handled about 5 million shares for around $8.3 million. Bank of America took a smaller position for about $2.5 million.

Separately, Pepsi bought $175 million of Instacart shares as a private placement on IPO day, a side deal negotiated outside the main offering. Goldman earned a 1.5% commission for facilitating that transaction, adding another $2.6 million. Goldman's total from the IPO came to roughly $18.5 million.

That is what bookrunners earn for taking on the risk, managing the logistics, and guaranteeing the company gets its money even if investor demand falls short.

The tension between analyst valuation and the market

Instacart had been valued as high as $39 billion during the private funding frenzy of 2021. By the time it went public in 2023, it repriced itself at $9.3 billion. That gap isn't just about the company performing worse. It reflects a shift in how markets were valuing growth companies overall, as interest rates rose and investors moved back toward profitability as a criterion.

This gap between what analysts or investors believed a company was worth at its peak and what the public market would actually pay is not unique to Instacart. It is a recurring feature of the IPO process, and it is part of why the timing of when a company goes public matters as much as the company's fundamentals.

The three-sided marketplace model is genuinely hard to build, requires significant capital to fund before it becomes self-sustaining, and operates in a structurally low-margin industry. Whether $9.3 billion was the right price for all of that depends on what you believe the advertising business can become.